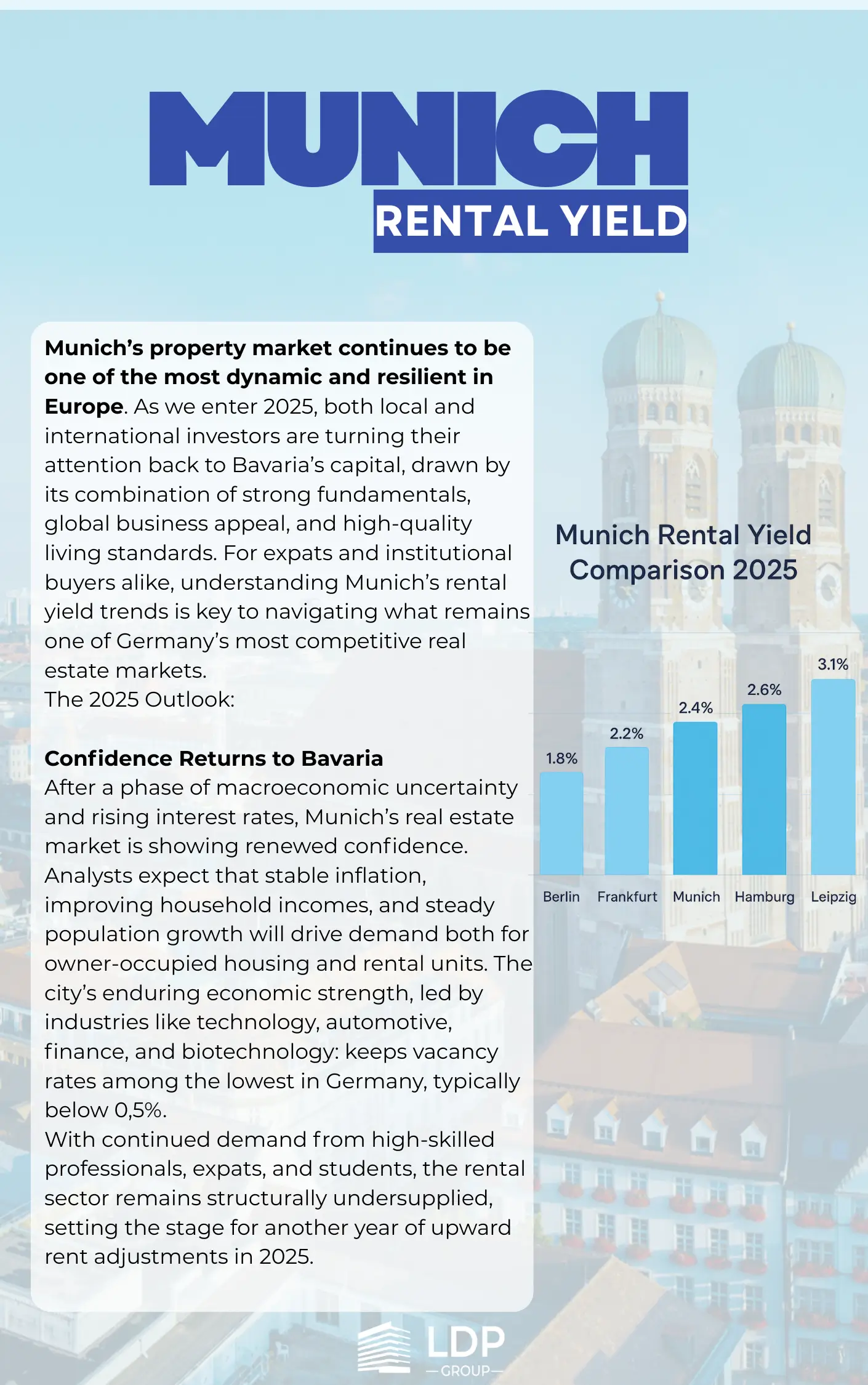

The Green Premium: Why Energy-Efficient German Property Pays Off for Expat Investors in 2026

Germany’s property market has fundamentally split in 2026 into two distinct tiers. Energy-efficient buildings rated A+ to B command rising premium valuations, while properties rated E, F, or G face mandatory retrofit costs and shrinking buyer pools. For expat investors, understanding this bifurcation and leveraging Germany’s generous energy-related tax incentives has become the single most important factor in real estate investment success. The era of buying any property and waiting for appreciation is over – the new winning strategy is energy class-driven asset selection paired with smart tax optimization.

- Capitalize on the rising Green Premium for energy-efficient assets.

- Leverage accelerated depreciation rates for KfW-Effizienzhaus properties.

- Avoid the retrofit cost trap that’s devaluing inefficient buildings.

Understanding the Green Premium in Germany’s 2026 Property Market

The German real estate market in 2026 is no longer a uniform asset class. Following the price correction of 2022-2024 and the subsequent stabilization, a clear two-tier market has emerged that fundamentally reshapes how expat investors should approach property acquisition. Energy-efficient properties rated A+ to B on Germany’s Energieausweis (energy performance certificate) are appreciating at rates of 4% to 6% annually in major metropolitan areas, while properties rated E, F, or G are being discounted by 15% to 25% relative to their energy-efficient counterparts. This divergence reflects buyer awareness of the mandatory retrofit costs imposed by Germany’s tightening Gebäudeenergiegesetz (GEG), the country’s building energy law.

Three powerful forces are driving this divergence simultaneously. First, the European Union’s Energy Performance of Buildings Directive (EPBD) requires member states to phase out the worst-performing buildings by 2030, with stricter standards by 2033. Second, rising energy costs have made operating expenses a major factor in tenant decision-making, with energy-inefficient rentals losing demand and commanding lower rents. Third, and most importantly for investors, German banks are increasingly reluctant to finance properties with poor energy ratings, often demanding higher equity contributions or refusing financing altogether for the worst classes.

For expat investors, this market split presents both unprecedented opportunities and significant risks. The same property that might have been a sound investment in 2020 could now represent a liability if its energy class is poor. Conversely, a slightly more expensive energy-efficient property can deliver superior total returns when factoring in lower vacancy rates, premium rents, eligibility for KfW subsidies, and accelerated depreciation. Understanding which side of this divide your investment falls on has become more important than location alone, and that’s why working with specialists who understand both the technical energy ratings and the tax implications is now essential for foreign investors entering the German market.

The Tax Advantage: Why Energy-Efficient Properties Multiply Wealth Faster

Germany rewards energy-efficient real estate investment through one of Europe’s most generous tax frameworks. For expat investors, the combination of accelerated depreciation, KfW subsidies, and energy-related deductions can transform what appears to be a modest yield property into a significantly more attractive after-tax return. The standard linear depreciation (Absetzung für Abnutzung) for residential properties built after 1924 is 2% per year over 50 years. However, properties certified to KfW-Effizienzhaus 40 standards qualify for substantially accelerated depreciation under §7b EStG, allowing investors to deduct an additional 5% annually for the first four years on top of the standard rate.

For a €500,000 building component, this accelerated depreciation translates to an additional €25,000 in deductible depreciation per year during the initial four-year phase – a substantial tax benefit that directly improves cash flow and overall investment returns. Beyond depreciation, the Kreditanstalt für Wiederaufbau (KfW) offers low-interest loans and direct grants for energy-efficient property acquisition and renovation. Programs such as KfW 261 provide financing at preferential rates with repayment subsidies that can reduce the effective loan amount by up to 25%, dramatically improving the equity multiplication effect for property investments.

Additionally, energy-related modernization expenses on existing properties can be deducted from rental income, or for owner-occupiers, claimed as a 20% tax credit over three years under §35c EStG. For expat investors strategically combining these incentives, the after-tax return on energy-efficient property can exceed that of conventional properties by 3 to 5 percentage points annually. The cumulative effect over a typical 10-year holding period is profound and often determines whether a German property investment delivers institutional-grade returns or merely matches inflation.

- Accelerated depreciation §7b EStG: 5% additional annually for first four years on KfW-40 properties.

- KfW 261 loans with repayment subsidies reducing effective borrowing costs.

- Energy-related modernization deductions reducing taxable rental income.

- §35c EStG: 20% tax credit on energy retrofits for owner-occupied properties.

- Lower vacancy rates and premium rents for high-efficiency assets.

The Retrofit Trap: Why Cheap Inefficient Properties Are Often the Wrong Choice

One of the most common mistakes expat investors make in 2026 is being attracted to the seemingly discounted prices of energy-inefficient properties. A building rated E or F might appear to offer 20% better entry pricing per square meter than its A-rated equivalent in the same neighborhood. However, this surface-level discount frequently masks substantial hidden costs that can erode or eliminate the apparent savings – and in some cases, leave investors with assets they cannot easily sell or finance when market conditions shift.

Mandatory retrofit costs under the GEG can range from €400 to €1,200 per square meter depending on the building’s current state and required improvements. For a 100-square-meter apartment, this translates to renovation costs of €40,000 to €120,000 – frequently exceeding the apparent purchase discount. These retrofits often include thermal insulation, modern heating systems (heat pumps are increasingly required), window upgrades, and ventilation systems. Worse, retrofits in existing buildings face structural and historical preservation constraints that can significantly increase costs or limit feasibility entirely.

Beyond direct costs, owners of energy-inefficient buildings face declining tenant demand, higher vacancy risk, and shrinking buyer pools when it comes time to sell. German tenants, particularly the younger professionals and international workers who form the core rental demand in cities like Berlin, Munich, and Frankfurt, increasingly screen properties by energy efficiency. A building rated F may rent for 10% to 15% less than a comparable A-rated property and experience longer vacancy periods. When compounding the price discount required at acquisition, ongoing operational disadvantages, and eventual exit challenges, the math for inefficient properties rarely works out for foreign investors who lack the local network to manage complex renovations efficiently.

LDP Group’s Approach: Identifying Green Investment Opportunities for Expats

Navigating Germany’s two-tier property market requires more than just understanding energy classifications. It requires the ability to identify undervalued energy-efficient properties before they fully reflect the Green Premium, structure financing to maximize KfW benefits, and integrate the investment into a broader tax strategy that captures every available incentive. LDP Group specializes in providing this end-to-end expertise specifically for international investors entering the German market, combining real estate intelligence with tax optimization in a way generalist brokers and tax advisors cannot.

Our investment screening process evaluates each potential property across multiple dimensions: current energy class and Energieausweis details, proximity to qualifying for higher classifications through targeted improvements, eligibility for accelerated depreciation under §7b EStG, applicable KfW program benefits, and rental demand projections specific to the property’s energy profile. We combine this technical analysis with location intelligence – for instance, identifying neighborhoods where infrastructure projects like Hamburg’s U5 expansion will compound value growth with energy efficiency premiums – to surface opportunities that single-factor analyses miss entirely.

A representative case study from our recent client work illustrates the impact of this approach. A US-based technology executive was initially considering a €420,000 apartment in Berlin Friedrichshain with an F energy rating that appeared to yield 4.2% annually. Our analysis revealed that mandatory retrofits within five years would cost approximately €85,000, while the property’s energy class would limit rental price growth and exit liquidity. We instead identified a €465,000 A-rated property in nearby Lichtenberg with a slightly lower headline yield of 3.9% – but once we factored in accelerated depreciation under §7b EStG, avoided retrofit costs, premium rental rates, and a KfW 261 loan with a 5% repayment subsidy, the after-tax internal rate of return over a ten-year holding period was projected at 9.4%, substantially exceeding the 5.8% projected for the inefficient alternative.

- Comprehensive energy class analysis combined with location intelligence.

- Strategic structuring to maximize §7b EStG accelerated depreciation.

- KfW program eligibility assessment and full application support.

- Integration with cross-border tax planning for expat investors.

- Ongoing portfolio optimization as energy regulations evolve.

Frequently Asked Questions: Energy-Efficient German Property for Expats

What energy class qualifies for accelerated depreciation in Germany?

Properties certified as KfW-Effizienzhaus 40, KFW-40 Plus, or higher standards qualify for accelerated depreciation under §7b EStG. This allows investors to claim 5% additional depreciation annually for the first four years, on top of the standard 2% linear depreciation, significantly accelerating tax benefits during the initial holding period. The property must meet specific technical standards and obtain the appropriate certification from a qualified energy assessor before depreciation can be claimed.

Can expat investors access KfW loans and subsidies?

Yes, KfW programs are generally available to foreign investors purchasing German property, though the application process typically requires working with a German bank as the intermediary lender. The investor does not need to be a German resident but must establish that the property meets KfW’s technical requirements through certified assessment. For expat investors, the application process benefits significantly from local expertise to ensure all documentation meets German banking and KfW standards.

How much can I deduct for energy retrofits on a German rental property?

For rental properties, energy-related modernization expenses are deductible from rental income, either as immediate operating expenses or as depreciation over the building’s remaining useful life, depending on the nature and scale of the work. Major energy retrofits typically must be capitalized and depreciated, while smaller repairs and maintenance can be fully deducted in the year incurred. For owner-occupied properties, §35c EStG provides a 20% tax credit on qualifying energy retrofit expenses distributed over three tax years.

What happens if I buy a low-energy-class property and don’t retrofit it?

Under Germany’s Gebäudeenergiegesetz, certain retrofits are mandatory upon property transfer or within set timeframes. Failure to comply can result in fines, but more practically, the property becomes increasingly difficult to rent, sell, or refinance. By 2030, EU regulations are expected to phase out the worst-performing energy classes entirely from active markets. Investors holding non-compliant properties face declining valuations, financing restrictions, and limited exit options when liquidity matters most.

Is the Green Premium already priced into the market, or is there still opportunity?

The Green Premium varies significantly by market segment and location. In prime A-city locations like central Munich or Berlin Mitte, the premium is substantially reflected in current pricing. However, in emerging B-cities, secondary neighborhoods within major cities, and properties undergoing or eligible for cost-effective energy upgrades, significant value gaps remain. Identifying these opportunities requires market-specific expertise and the ability to evaluate properties on energy retrofit potential alongside current energy class.