Turning Taxes  Into Wealth with German Real Estate

Into Wealth with German Real Estate

60+ Million

in annual Transaction Volume

1000+

Clients consulted

5 Languages

EN · DE · AR · HI · TA

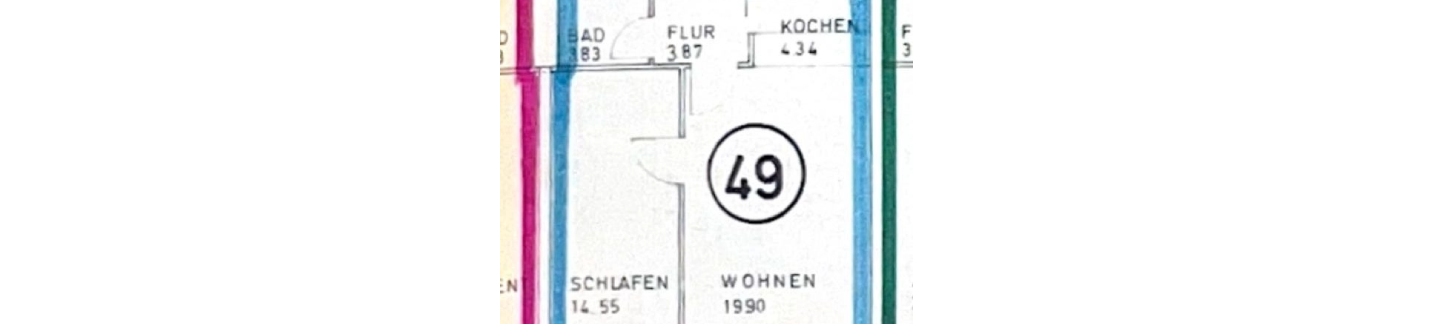

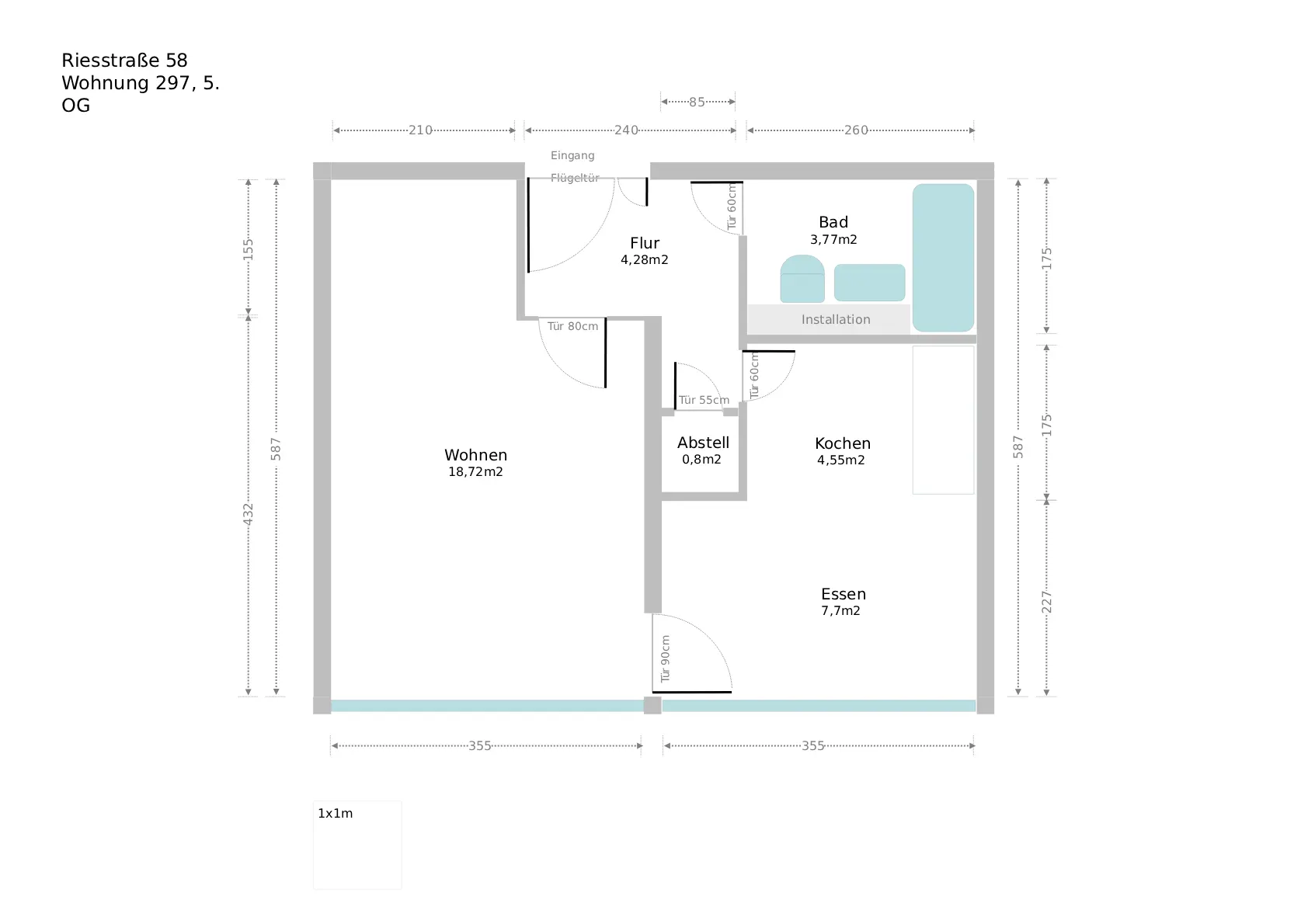

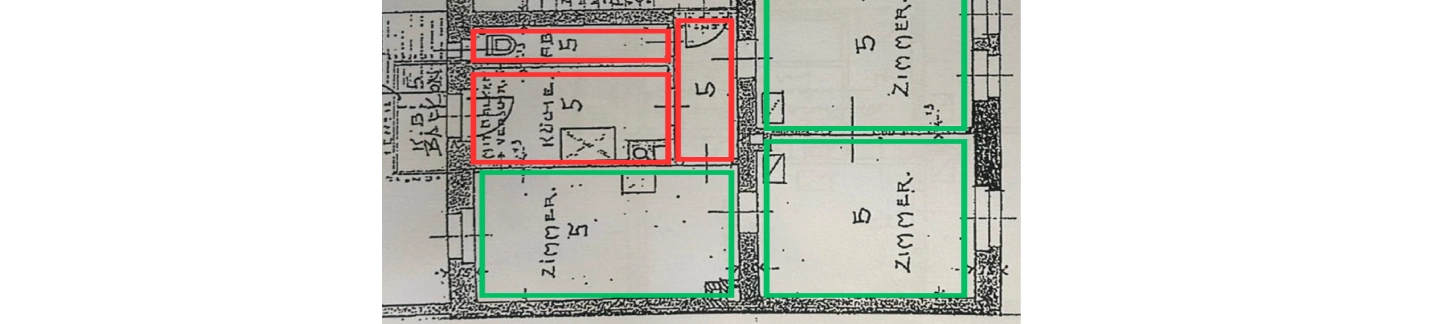

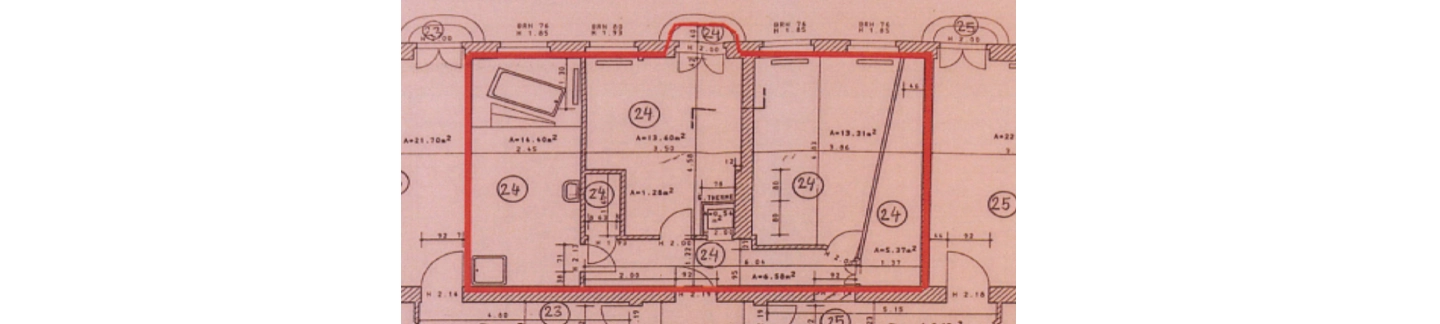

Investment Property

63SQM

63SQM$567,000

Voltastraße 21, 13355 Berlin

2 bathrooms

2 bathrooms  4 bedrooms

4 bedrooms 60+ Million

in annual Transaction Volume

1000+

Clients consulted

5 Languages

EN · DE · AR · HI · TA

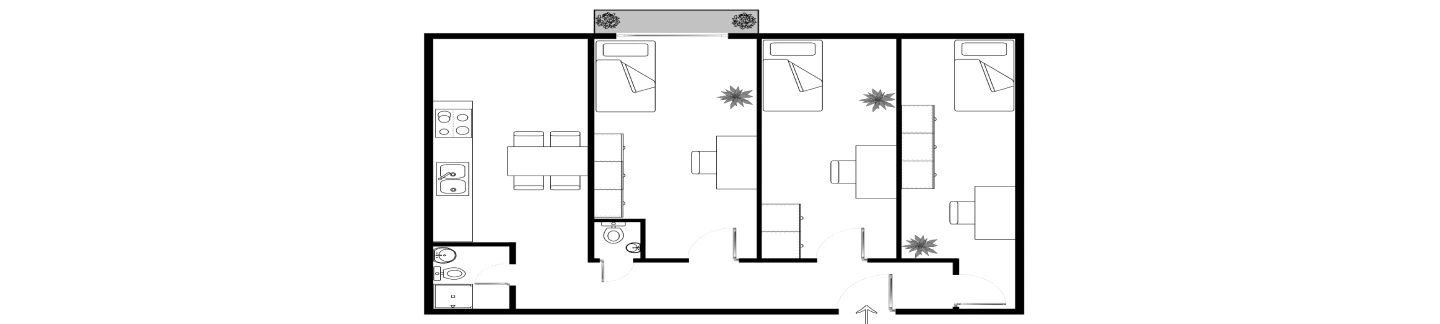

LDP Group

Appenzeller Str, Munich

Appenzeller Str, Munich